Nikkei 225 index Funds, Should I buy the Nikkei and Why I Only Recommend Putting a Small Portion of Your Portfolio Into This Popular Japanese Index

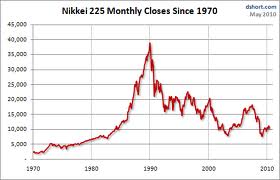

In this blog post, yes you just read that correctly, I am going to talk about Nikkei 225 index funds, and am going to go through why exactly I think this is a great index to add some foreign exposure to an otherwise country-specific and home country biased portfolio, but why global index funds are probably the better solution, and of why I would probably only make the Nikkei something like 7-10% of your total portfolio. The gist of why I say not to put too much money into the Nikkei 225 is that the Japanese stock market was the stock market that has recently taken off (in the past five years or so) but that I seem to remember having something like a 10 or 20 year hiatus of complete stagnation where investors in this Japanese stock index made virtually no money at all just because of the timing and the time period that they chose to hold this index in. And so, once again, in this blog post, let’s talk about the Nikkei 225, read on or comment down below for more details and information.

Some other top indexes worth looking at for additional foreign exposure include:

The S and P 500

Popular Canadian Indexes

FTSE All World Index

VT, The Vanguard Total World Stock Market Index

Dow Jones Global Titans 50

S and P TSX Composite Index

Capitalization Index

The VIX

The Fear Index

The Consumer Price Index

TSE 300

Wilshire 5000

And a host of other popular indices, read on or subscribe to our blog for additional details and information.

Should I Buy Nikkei 225 Index Funds, Why or Why Not?

| Related Posts |

|---|

So, once again, yes and no. I typically recommend sticking with US, Canadian or Global Stock Index funds for the vast majority of your portfolio, and usually these should be as close to the total market index in your country of chosen preference as possible (for instance, using the Wilshire 5000 or the S and P 500 for a United States representation instead of something like the Dow Jones Industrial Average or the Russell 2000, which are much less diversified and more volatile than the aforementioned indices.) I also recommend sticking with US, Canadian and Global Index fund stock baskets because I think that these are the countries and funds most likely to continue growing their GDP, economies, and thereby their stock markets at say the standard 7-10% annualized rate of return that we have become so accustomed to. I feel that with the Asian markets, such as the Nikkei and the Chinese markets, that it is much more volatile and more of a wildcard, and that I would only put a small percentage of my portfolio in them over the long haul in order to increase my foreign exposure and increase my international diversification benefits marginally.

Nikkei 225 Index Funds, The Top Ten Japanese Stocks in This Popular Index Fund

And so, in the relative closing portion of this blog post, here are the top ten largest Japanese stocks within the Nikkei 225 index:

- Dai Ichi Life Insurance

- Sanyko

- Daikin Industries

- Daiwa House Industries

- Advantest

- Aeon

- Ajinomoto

- Alps Electric

- Amada

- Chubu Electric Power

And a host of other companies, the largest companies in the Nikkei are definitely much different than those of the US, which is comprised almost entirely of tech stocks (Tesla, AMZN, Microsoft, Apple, Google, etc.)

Final Thoughts on Holding Nikkei 225 Index Funds as a Small Portion of Your Portfolio

And so, in reiterating the main focal point of this blog post, I would recommend only holding the Nikkei 225 index fund, or any Asian markets for that matter, in very small portions of your total portfolio. They can be a great inflation hedge and a fantastic way to add international exposure to an otherwise biased portfolio, however they have also been known to be very volatile, so be careful with this. For more information, read on or subscribe for more articles!

Cheers!

*Inflation Hedging.com

Sources:

https://www.bankrate.com/banking/cds/cd-rates/

https://money.cnn.com/data/markets/

Disclaimer: The opinions and documentation contained within this article and on this blog are the sole property of inflationhedging.com and are not to be copyrighted or reproduced in any manner, else legal action within the rights of the United States legal code could be use to obtain recompense. All articles and blog posts are the sole opinions of the writers of the blog, and are not necessarily in line with what exactly will work for you, you should consult a CPA, Tax Professional, or Financial Professional to determine what exact financial needs are in line with your interests. Also, from time to time, certain links on this website will be used to generate affiliate commissions, in order to support the health and growth of our website, health and business.

[…] Previous Charcoal Toothpaste Walmart Prices, Benefits of Charcoal Toothpaste […]

[…] my blog post review of the scene where Harvey subpoenas Mike at the bar, I’ve just got to start out by saying […]

[…] absolutely obsessed with for two very different, although somewhat similar fields, the fields of Finance and SEO. I have heard things like it takes 1,000 hours to become an expert in your field, it takes […]