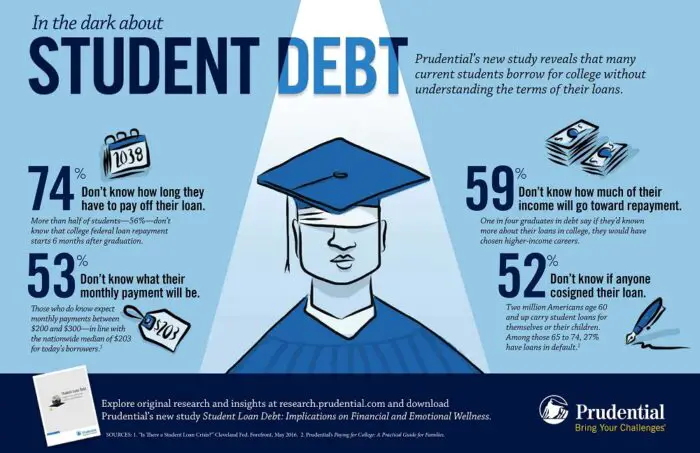

Why Can’t You Discharge Student Loans in Bankruptcy? My Opinion And Other Types of Debt That Can’t Be Declared In Bankruptcy

Why can’t you discharge student loans in bankruptcy? Generally speaking student loans cannot be discharged in Chapter 7 Bankruptcy. I just finished my Business Law for Accountants class and they had a vast description of bankruptcy law within the course, so I thought it prudent to give a description of the types of debt that you can get rid of, and which types you cannot. I will not discuss the dangers of Student Loans here and why they are so catastrophic financially, insomuch as I have written about this at length in a prior section. Instead, let’s look at what types of debt is dischargeable and why.

A great Tax CPA friend of mine once said that “logic and the tax code do not make sense. Don’t try to apply logic to learning the tax code because there is essentially nothing logical about it. The tax code is about social engineering it’s not about logic.” I think that, from what I have read so far, bankruptcy law is much the same in this instance. Think of bankruptcy law in terms of sociological reasons more than logical ones.

Here are the types of debt that cannot typically be discharged in bankruptcy and the socioeconomic reasons behind these bankruptcy disallowances:

Student Loans

Tax Debt

Tax Debt

Alimony and Child Support Debt

Mortgage Debt (Secured)

Automobile Debt (Secured)

Debts from any sort of Fraud

Debts from Tortious Conduct or a Court judgement against you

Debts for luxury goods or services bought 90 days before filing

Debts from breach of fiduciary duty

SALT taxes

Government penalties

Court Fees

Legal Fees

CPA Fees

Debts that were determined non-dischargeable in a prior bankruptcy

401K loans or debts owed to certain pension plans

Debts for HOA fees for Condo Dues

Debts not dischargeable in a prior bankruptcy due to fraud or inability to properly file on time.

Debts from a Divorce Decree or Settlement

| Related Posts |

|---|

Why Can’t You Discharge Student Loans In Bankruptcy Specifically? Or can You After All!

The one interesting thing about Student loans with relevance to this list is that they almost seem like an outlier. Everything else is usually malicious intent or bad mistakes like divorces, whereas the student loans in this area seem completely out of place. Turns out that there are actually some cases where these can be discharged, such as if “the court finds that paying off the loan will impose an undue hardship on the debtor and dependents.”

Sounds like to qualify for this, you have to show that you cannot make the payments for this at the time bankruptcy is filed.

*****Quick disclaimer on this blog post, I am not a lawyer and this should not be misconstrued as legal advise. I am a hopefully future CPA in the next few years that is writing this on my business blog out of pure fun, please consult an attorney if you plan on going to bankruptcy court.

Final Thoughts On Why I Think The Above Is True of Bankruptcy

Bankruptcy is not some magic wand that gets you away from all of your financial obligations. As a matter of fact it is actually extremely difficult to get stuff charged in bankruptcy, and the courts typically uproot your entire life as you go through the bankruptcy process and get debts wiped out. It is typically for non student loan, non-alimony, non fraudulent debt that is unsecured debt like credit cards. Aside from this, you are almost better off, at least in my humble, non legal opinion, just paying down the debt yourself with the money you have, rather than going to bankruptcy. Hope you enjoyed reading and be sure to subscribe!

Sources:

https://www.bankrate.com/banking/cds/cd-rates/

https://money.cnn.com/data/markets/

Disclaimer: The opinions and documentation contained within this article and on this blog are the sole property of inflationhedging.com and are not to be copyrighted or reproduced in any manner, else legal action within the rights of the United States legal code could be use to obtain recompense. All articles and blog posts are the sole opinions of the writers of the blog, and are not necessarily in line with what exactly will work for you, you should consult a CPA, Tax Professional, or Financial Professional to determine what exact financial needs are in line with your interests. Also, from time to time, certain links on this website will be used to generate affiliate commissions, in order to support the health and growth of our website, health and business.

[…] Previous What Does God Think of Rich People? […]