How Much Does A Hard Credit Pull Lower Your Score? How to Reduce This over Time

How Much does a hard credit pull Lower your credit score, and how can you get this back up or avoid this depending on what you overall credit is? In today’s blog post, that’s right, we’re going to talk about credit scores and your credit report, of why updating it and keeping it up to date with regards to income, addresses and past jobs is an important thing to do, and of why you should always make time for checking up on your own personal finances. So, the gist of how much a hard credit pull is going to lower your credit score, is that it is somewhere in the range of 10 to 30 points depending on how much credit history you have, and of how strong your credit score and your credit report is to begin with. For instance, if you only have 3 years of credit history with a 550 FICO score, yes getting hit with a hard credit pull from say a new credit card application or apartment lease, is going to bring your score down by a lot and for awhile, it may give you as much as a 30 point hit. Whereas someone with a 775 credit score will likely only fall to like a 760 or a 750 credit score and only for a short period of time. And so, in this blog post, I’ll be explaining how credit works!

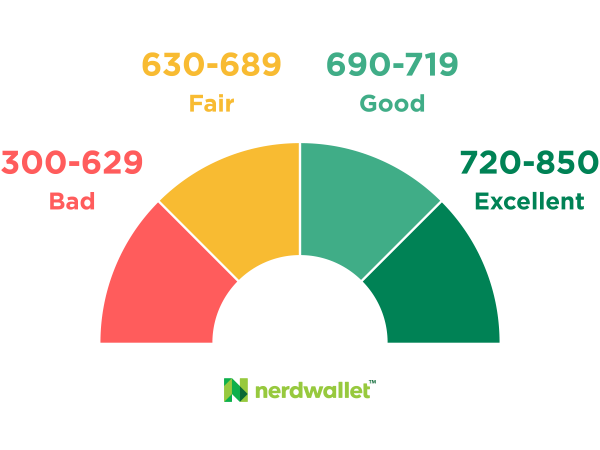

Here’s my definition of the credit scores table:

450 Credit Score – Terrible credit score, this is pretty much the worst possible credit score you could ever imagine, get all the way down to this and you’ll quite literally never get credit again.

500 Credit Score – Ditto on a 500 and 450 Credit Score.

550 Credit Score – 550 Credit Score is the typical moderately bad credit score. You can still get an apartment with this, but its right on the line.

600 FICO Score – This is starting to get into decent credit here, you might have this when you just start, or if you’ve missed a few payments or defaulted on a car loan or something.

650 FICO Score – This is getting into either decent credit recovery, or if you are just starting out with a blank slate.

700 Credit Score – Take out a car loan and a credit card and never miss a payment, and build up credit lines and get 5 years of credit history, and this is where you’ll be.

750 Credit Score – Same here.

775 Credit Score – Multiple loans with a good credit history of paying everything back can get you here, from here the longer you keep the average age of your credit cards, the more your score will go up from here. Get some credit cards in your early 20s and don’t apply for anymore, keep all the balances low or at 0 and you can ascend to the 800+ credit score ranks.

800 Credit Score – See above explanation for 775 credit.

| Related Posts |

|---|

850 Credit Score – See above.

Why Credit Score Matters, How Much Does a Hard Credit Pull Lower Your Score?

So, your credit score matters for a lot of reasons, and is pretty much going to be a large part of your overall financial situation until you hit a number in your bank account that is so high that you don’t have to care, like say the $4,000,000.00 mark, from here, you’d still get credit even with like a 550 FICO. So your credit score is important for leasing a car, for getting credit extended to you in case your debit card is stolen etc. for working in certain financial jobs, for getting an apartment rental, for getting a mortgage extended to you, etc. etc. Your credit score will most likely, even if you are very debt averse like I am, play a major factor in what you are allowed to do in your life overall.

Final Thoughts on Why a Hard Credit Pull Lowers Your Score, My Final Opinion

A hard credit pull is going to lower your credit score in that they want to discourage people from just signing up for tons of credit cards at one time, as well as a host of other reasons. Overall, your credit score is something that is going to be very important to your overall lifestyle and financial future, be sure to always make your payments on time, and to always do whatever possible to give yourself a good credit score. Until next time, you heard it first right here at Inflation Hedging.com.

Cheers!

*Inflation Hedging.com

Sources:

- https://medium.com/nori-carbon-removal/how-i-passed-the-securities-industry-essentials-sie-exam-de86529f9feb

- https://www.professionalexamtutoring.com/sie-exam-difficulty/

- https://www.efinancialcareers.com/news/evergreen/seven-tips-for-acing-the-series-7-and-other-financial-exams

Disclaimer: The opinions and documentation contained within this article and on this blog are the sole property of inflationhedging.com and are not to be copyrighted or reproduced in any manner, else legal action within the rights of the United States legal code could be use to obtain recompense. All articles and blog posts are the sole opinions of the writers of the blog, and are not necessarily in line with what exactly will work for you, you should consult a CPA, Tax Professional, or Financial Professional to determine what exact financial needs are in line with your interests. Also, from time to time, certain links on this website will be used to generate affiliate commissions, in order to support the health and growth of our website, health and business.

Leave A Comment